Payplan Cover My Life CML Scams.

What I Learned About PayPlan’s “Cover My Life” After 14 Years: A Consumer’s Discovery Journey.

After 14 years on a Debt Management Plan, I finally reviewed PayPlan’s “Cover My Life” add‑on. Here’s what I discovered about how the product was described, what information I could and couldn’t find, and the questions I’ll be asking PayPlan next.

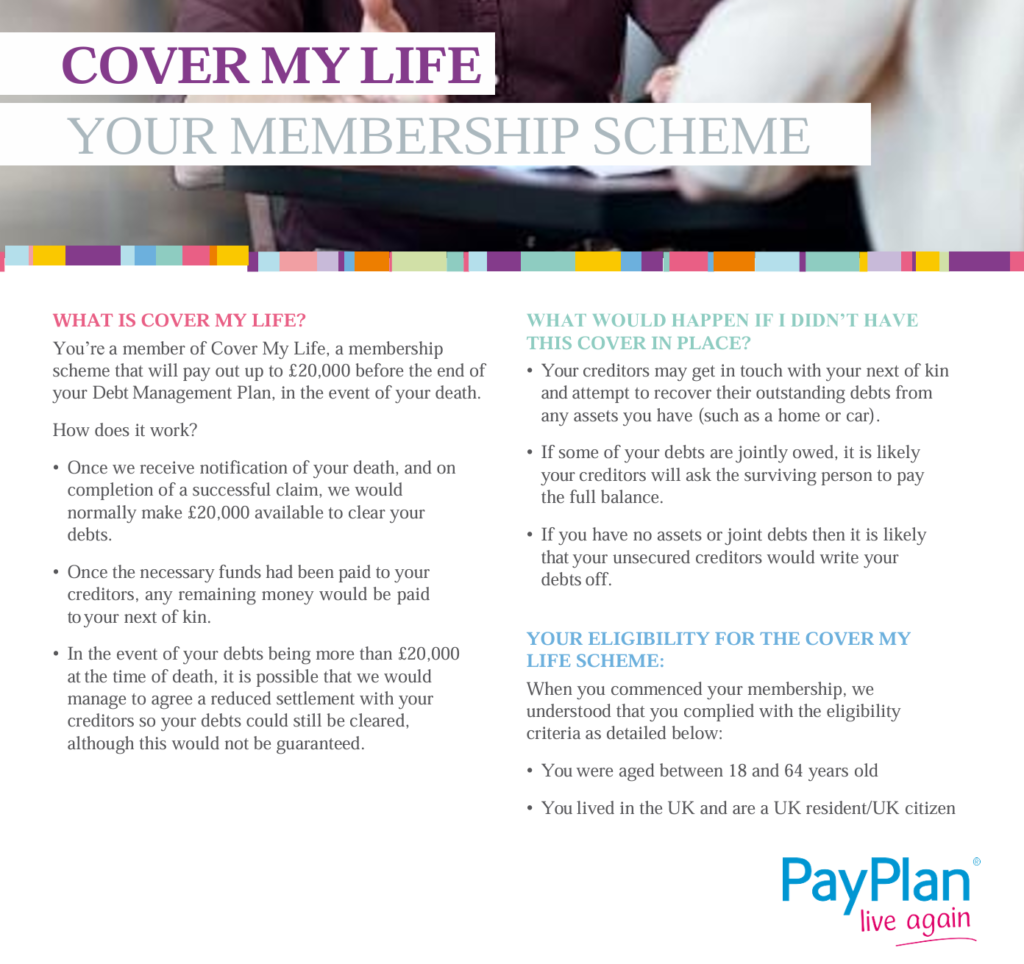

Age Restrictions I Noticed in the CML Leaflet

One thing that stood out to me when reviewing the CML leaflet was the age restriction. The leaflet says that only people aged 18 to 64 could join the scheme.

Age limits are common in insurance products, but CML wasn’t an insurance policy — it didn’t have an underwriter, a policy number, or a claims process. So the use of an insurance‑style age restriction raised questions for me about how the product was intended to work and why this particular eligibility rule was used.

This isn’t a criticism — just something I noticed when reviewing the documentation.

What I Learned About PayPlan’s “Cover My Life” After 14 Years

Payplan Cover My Life CML Scams, my own story. For more than a decade, I paid for just one add‑on products alongside my Debt Management Plan: Cover My Life (CML) I didn’t question that at the time. I trusted the advice I was given, and like many people in long‑term financial difficulty, I simply focused on keeping my head above water.

Only in the last few months did I finally sit down and try to understand what these products actually were.

This post isn’t an accusation. It’s simply a record of what I discovered — and when I discovered it.

A Calm, Clear Summary of What I Found

Over the last few days, I learned more about CML than I had in 14 years. Here are the key things that stood out to me:

- The product was described in Ombudsman summaries using death‑triggered language (“in the event of your death”).

- I couldn’t find any claim form, claims process, or membership/policy number in my documents or online.

- The product leaflet I have uses a fixed £20,000 figure, not “up to £20,000”.

- I only recently learned that unsecured debts are written off automatically when someone dies — something I was never told at the time.

- I couldn’t find any next‑of‑kin process, even though the leaflet mentions next‑of‑kin.

- My address was incorrect for years, so I never received certain letters that are referenced in Ombudsman cases.

None of this is a claim of wrongdoing. It’s simply what I found when I reviewed my own paperwork.

What This Post Is: A personal account of my own experience reviewing my paperwork after 14 years on a DMP, and the questions I now have.

What This Post Isn’t: It isn’t an accusation, allegation, or claim of wrongdoing. It isn’t legal advice. It isn’t a complaint. It’s simply my discovery journey.

Timeline of Discovery

This is important for context — especially if I later raise questions formally.

2007–2024:

- I paid for CML and CMP monthly.

- I didn’t understand the products beyond “extra protection”.

- I never received any detailed explanation of how they worked.

- My address was incorrect in PayPlan’s system for years.

June 2026 (This Week):

- I read an Ombudsman summary online that described CML as a death‑triggered benefit.

- This was the first time I realised CML was framed this way.

- I searched for a claim form — I couldn’t find one anywhere.

- I checked my DSAR documents — no claim form, no claims process, no next‑of‑kin form.

- I checked the CML leaflet — it uses a fixed £20,000 figure.

- I learned (for the first time) that unsecured debts are written off automatically when someone dies.

- I realised I had never been told this during my DMP.

- I realised my family would never have known about CML, and PayPlan never collected next‑of‑kin details.

This is why I’m only now in a position to ask questions.

Many people on long‑term DMPs sign up to add‑on products without fully understanding them.

Life circumstances, stress, disability, and financial pressure can make it difficult to question things at the time.

Reviewing old paperwork can help people understand what they were paying for and whether they received the information they needed.

What I Couldn’t Find

When I reviewed my documents and searched online, I couldn’t find:

- any CML claim form

- any claims department

- any claims email or phone number

- any next‑of‑kin form

- any death‑notification process

- any membership or policy number

- any explanation of how a claim would be made after death

This doesn’t prove anything by itself — but it raised questions for me as a consumer.

What Surprised Me Most

1. The death‑triggered wording

I had never been told CML was described this way.

2. The fixed £20,000 figure

The leaflet uses a universal £20k amount, not “up to”.

3. The lack of a claims process

I couldn’t find any documentation explaining how a claim would be made.

4. The next‑of‑kin issue

The leaflet mentions next‑of‑kin, but I was never asked for any details.

5. The debt‑write‑off rule

I only learned this week that unsecured debts are written off automatically on death.

If you were ever on a DMP and paid for add‑on products, here are some steps you can take:

- Check your DSAR for any product leaflets or explanations

- Look for a claims process or membership number

- Check whether you were ever asked for next‑of‑kin details

- Review whether you received annual suitability reviews

- Make a list of anything you don’t understand

This isn’t about blame — it’s about understanding your own paperwork.

Questions I Will Be Asking PayPlan

I’m not making accusations — I’m simply seeking clarity.

Here are the questions I plan to ask:

1. How was CML intended to work in practice?

What was the operational process behind the product?

2. How would a claim be made after someone’s death?

Was there a form, department, or procedure?

3. How were next‑of‑kin supposed to be identified or contacted?

Was there a system for this?

4. Why does the leaflet use a fixed £20,000 figure?

Was this universal for all customers?

5. Why was I never told that unsecured debts are written off automatically on death?

This seems like important information for understanding the product.

6. Why was my address incorrect for so many years? (14 years).

This affected what letters I did or didn’t receive.

7. Were annual suitability reviews carried out?

If so, what did they involve?

8. What information was I supposed to receive about CML?

And when?

These are reasonable, calm, factual questions — nothing more.

My next step is simply to contact PayPlan and ask the questions listed above.

I’m not making any assumptions — I just want clarity.

Once I have their answers, I’ll decide whether I need to take things further.

Why I’m Sharing This

I’m sharing this because:

- I only learned these things recently

- I want a clear record of my discovery

- I want to understand what I was paying for

- I want to ask informed questions

- I want to help others who may be in the same position

This is not about blame. It’s about clarity.

Final Thoughts

For 14 years, I paid for something I didn’t fully understand. In the last few days, I’ve learned more than I ever knew before.

This blog post is simply my way of documenting that journey — calmly, factually, and without making any claims about anyone’s conduct.

If you’ve ever been on a DMP and paid for CML or CMP, it might be worth reviewing your own paperwork too. Not to accuse anyone — just to understand what you were paying for.

Knowledge is power. And I only just got mine.

If you enjoyed this content you will love what we are doing over at our sister website Probate Scams Website.

Post Tags; Debt Management Plans, Consumer Education, Financial Awareness, PayPlan, CML, Debt Help, DSAR, Long‑Term Debt